Oct 16, 2020

Why Bitcoin sidesteps OKEx Freeze

Uncertainty continues after withdrawals resume, though BTC hit remains moderate

Not so OK

Unfortunately, it’s been another day on tenterhooks for retail crypto traders. The latest in a string of exchange debacles this year involves OKEx, the Malta-based venue which has deeper roots in Hong Kong and China.

As is often the case when digital asset exchanges run into trouble, news trickled out slowly and erratically, exacerbating market nerves and, in turn, prices.

With OKEx, things began as ominously as they commonly do in situations like these with customers suddenly unable to withdraw funds. It later emerged that the firm had suspended withdrawals. Later still, that this was due to the absence of a “private key holder”.

Co-operating

Finally, it emerged that the person was none other than founder Xu Mingxing. Reports said he was “co-operating” with Chinese authorities in a government investigation. It remained unclear at the time of writing whether or not Xu had been arrested after local reports indicated that he had been ‘taken away by the police’.

The exchange stressed that withdrawals were halted with the “best interests” of customers in mind whilst assuring that aspects of business were “stable”, and that asset security was unaffected. Late on Friday, there was anecdotal evidence that withdrawals had resumed.

No melt-down

Unsurprisingly, the market’s knee-jerk reaction was negative. Still, both the price and volume response warrant careful scrutiny, because to be sure, there was no ‘melt-down’.

As the chart of CF Benchmarks’ Bitcoin Real Time Index (BRTI) shows, traders of the main cryptocurrency demonstrated a clear selling reflex following emergence of the OKEx news in the form of an announcement on the firm’s website on Friday at around 0400 UTC.

Figure 1 – CME CF BRTI – 04:00 – 07:00 UTC – 16-10-2020  Source: CF Benchmarks

Source: CF Benchmarks

That said, prices of the regulated BRTI index, at worst, fell less than 3% in the immediate aftermath of the news. Likewise, Bitcoin traded around 0.9% lower at the time of writing, several hours after the initial news. BRTI receives data from five meticulously selected and regularly reviewed constituent exchanges before a painstaking methodology and stringent controls are applied to derive price. The determinations are all part and parcel of the EU’s BMR rules that govern CF Benchmarks status as an official benchmark administrator. So, if the BTRI fell less than 3% in reaction, it corroborates the impression that the market impact was negative but essentially moderate.

Volume verdict

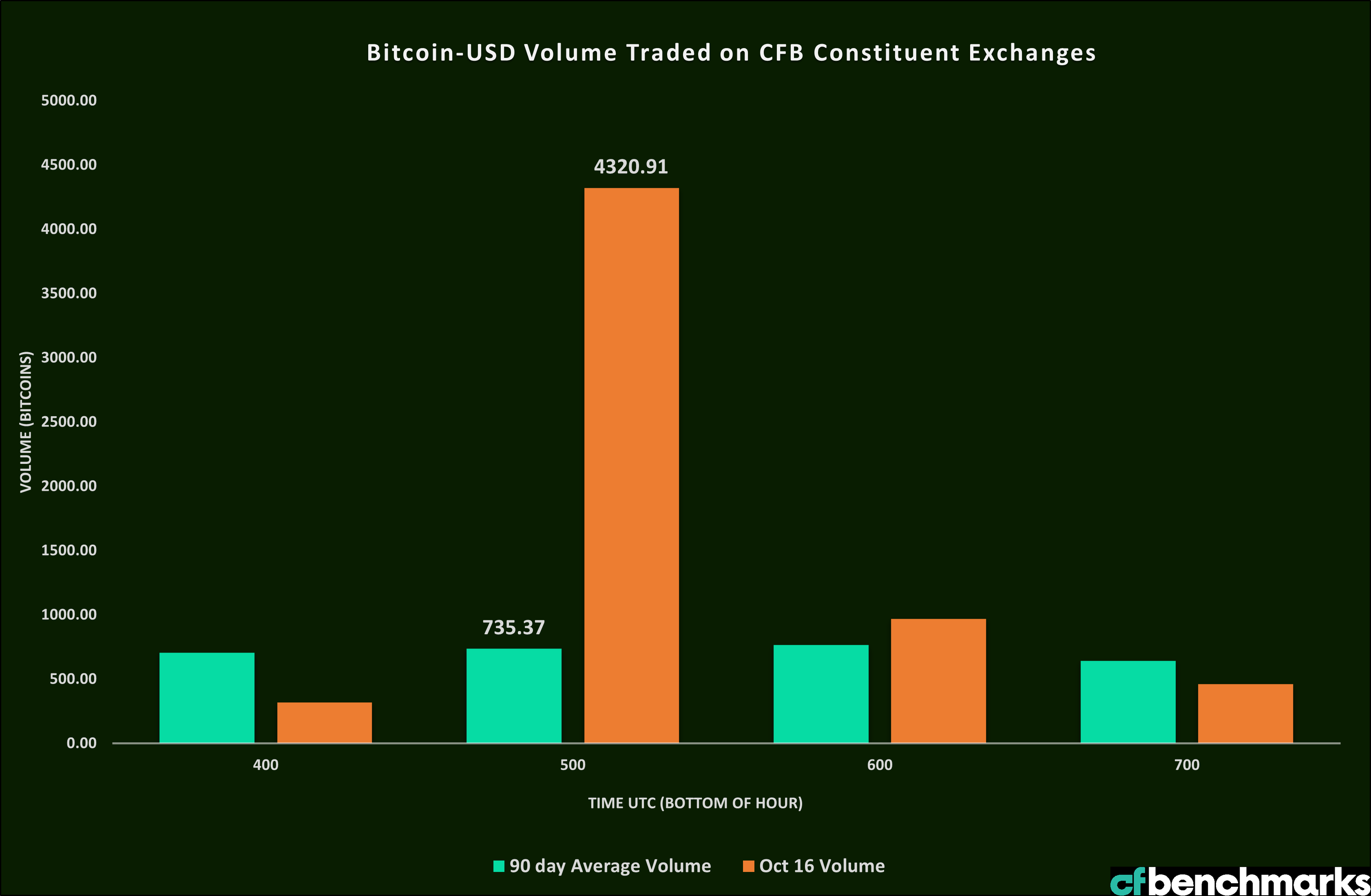

Benchmark volume data provide a further level of insight. The next chart shows an almost six-fold surge in BTC-USD volume relative to its 90-day rolling average. However, activity soon reverted back to its previous approximate baseline. We can interpret that as indicating that participants certainly did not ignore the OKEx news. However, it’s also clear that traders rapidly assessed the prima facie risks tied to the revelations and their working verdict appears to be that consequent impacts are likely to be contained; albeit OKEx customers are probably less sanguine.

Figure 2. – XBT-USD hourly volume – 0400 UTC – 0700 UTC – 16-10-2020 Source: CF Benchmarks

Source: CF Benchmarks

Reality check

As much as the crypto industry has made great strides this year, particularly in terms of mainstream adoption, messy let-downs like Friday’s are no less common and continue to serve as a reality check to the crypto industry, retail consumers and the broader markets alike.

Still, contained OKEx impact speaks to the diminished influence of the Malta-registered venue (and Seychelles-registered BitMEX) on the crypto derivatives market in 2020. There are now more than a dozen such vendors in that asset class to choose from compared to a few years ago when the pair dominated trade.

Familiar lessons

Whilst details around the OKEx freeze continue to emerge, the latest example of crypto exchange disruption already reaffirms basic lessons from numerous other instances—including BitMEX.

- Consumer pain tends to be much reduced with exchanges regulated onshore compared to those regulated offshore

- As crypto markets (and perhaps typical behaviour patterns) mature, wider choice and inevitable regulation are likely to continue to mitigate the impact of crypto exchange SNAFUs, though the frequency of their occurrence shows little sign of decreasing for now

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Ken Odeluga

Ken Odeluga