Dec 11, 2024

CF Benchmarks introduces first Institutional-grade Factor Model for Digital Assets

Debunking the myth of crypto’s Random Walk: our quantitative research shows liquid market returns mirror traditional market dynamics

Institutions eye Crypto Factors

Surveys over the past decade have shown that the use of factor-based strategies by institutional investors in their investment processes is widespread and continuing to grow.

The trend is prevalent across the two broad traditional market asset classes of equity and fixed income, with evidence of increasing interest in factor-based credit strategies also readily available.

This represents a remarkable proliferation of factor-based strategies, considering that widespread adoption of quantitative factors as part of the portfolio management process is known to be directly linked to the relatively recent publication of key research in the field; chiefly the Fama-French Three-Factor Model in the early 1990s.

The extensive and increasing utilization of factors by institutions managing traditional assets suggests this investor cohort will seek to deploy factor-based strategies for the management of digital assets as well, particularly given the significant adoption of crypto by major financial firms seen in recent years.

The Challenge of Validation

That said, attempts to do so are unlikely to be free of friction. The substantial discontinuity between the characteristics of traditional asset classes and those of the digital asset class mean that factor strategies applicable to the former cannot simply be copied and pasted on to portfolio management systems for the latter.

It’s likely that even relatively large traditional institutions simply do not possess the installed base of expertise required to undertake the breadth of research necessary for potential validation of factors embedded in the digital asset class.

Meanwhile, the relatively narrow range of reliable crypto market datasets available is another challenge.

Nevertheless, it is axiomatic that the same broad benefits of factor-based strategies, evident in their use with mainstream assets, are certain to be engendered if such approaches were to be utilized within crypto.

These include the delivery of long-term risk premia, reduced overall portfolio risk, increased transparency during portfolio construction and management, and improved understanding of past and future drivers of returns.

It is for this reason that CF Benchmarks, the registered Benchmark Administrator and world’s largest provider of regulated crypto pricing sources, by assets under reference, has conducted the most extensive quantitative analysis of validated crypto data sources for the investigation of factors applicable to the digital asset class.

We now present our findings in a comprehensive research report:

A Factor Model for Digital Assets

What the paper says: a summary

Introduction

The paper focuses on developing a quantitative framework to assess risk factors in cryptocurrencies, leveraging insights from mathematics, finance, and technology. The study proposes a factor model tailored to digital assets, aiming to bridge the gap between traditional investment frameworks and the nascent cryptocurrency market. By focusing on risk management and portfolio optimisation, the authors seek to empower investors with reliable tools for navigating the digital asset space, as demonstrated concisely by the excerpt below:

“This investigation holds substantial value for several reasons. While stocks and bonds benefit from decades of research and empirical evidence, cryptocurrencies remain relatively uncharted territory. By bridging this gap, our work can empower investors with reliable tools to navigate digital asset markets. Furthermore, cryptocurrencies exhibit extreme volatility, making risk management crucial. Quantitative models can help identify risk factors, optimise portfolios, and enhance decision-making. Our research contributes directly to optimising portfolios and managing investment risks specific to digital assets.”

(From Section 1. Introduction, paragraph 4)

Literature Review

Traditional Assets

The review traces the evolution of risk factor models from Markowitz's portfolio theory to the Fama-French multi-factor models. These frameworks highlight factors like size, value, and momentum in predicting stock returns. The Arbitrage Pricing Theory (APT) extended these ideas by incorporating multiple macroeconomic risks. These developments underscore the importance of systematic approaches in financial markets.

Crypto Assets

Cryptocurrency pricing research highlights factors like size, momentum, and blockchain-specific metrics, which includes on-chain data such as transaction fees or network activity. As such, these emerging models integrate traditional and novel factors to explain cryptocurrency returns better.

Data

The data framework leverages “a broad scope of CF Benchmarks sourced data and resources to ensure a comprehensive examination of data quality.” Data environments utilized include exchange APIs, blockchain nodes, and open-source tools to gather transactional and on-chain metrics such as transaction fees, Total Value Locked (TVL), or active user metrics, among others.

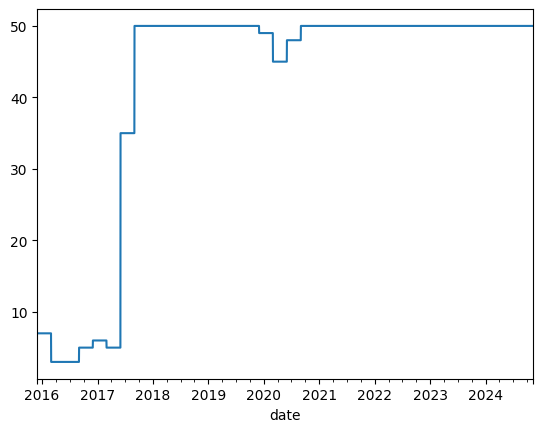

With these data in hand, the study focuses on the top 50 cryptocurrencies by market capitalization, whilst excluding stablecoins, derivatives, and other pegged assets, in order to ensure data reliability.

An illustration of the estimated universe can be seen in the excerpted graphic with accompanying text reproduced below.

“Figure 1 shows the number of assets that satisfy our estimation universe selection criteria on each universe snapping date. In the early years, like 2016 and 2017, we could not find enough assets with sufficient liquidity. However, as crypto assets have evolved over time, liquidity has become less of an issue, allowing us to find all 50 assets satisfying our criteria in recent years.”

(From Section 3. Data, 3.1, Universe Estimation, paragraph 5)

Methodology

The authors propose a robust set of factors derived from digital asset data. The methodology integrates the three broad steps summarized below, into a research methodology than can be summarized thus:

- Evaluation of descriptors for the identification of robust factor candidates

- Combination of descriptors into style factors for factor portfolio construction and risk premia identification

- Construction of factor models from various regression analyses, leveraging isolated factor sets for the assessment of model significance

Here are concise descriptions of each step in the research methodology:

- Descriptors: Using price-volume metrics and on-chain data to identify return drivers

- Factors: Key factors include market, size, value, momentum, growth, downside beta and liquidity

- Factor Models: Applying time-series and cross-sectional regression methods (e.g., Fama-French and Fama-MacBeth) to quantify factor contributions to return variations

Factor Definitions

Following an analysis of the raw descriptor data, factor portfolio returns and perceived narratives for digital asset markets corresponding to traditional factor models, the following isolated factors exhibiting significant risk premia emerged: Market, Size, Value, Momentum, Growth, Downside Beta and Liquidity.

The authors qualify these labels with respective endogenous characteristics from their emergence in the digital asset as follows:

- Market: Measured as a Bitcoin-Ethereum weighted index

- Size: Derived from market capitalization

- Value: Captured as the combined ratios of Fees to TVL and Daily Active Users (DAUs) to Market Capitalization

- Momentum: Based on short-term historical returns

- Growth: Focuses on fees and DAU growth over time

- Downside Beta: Captures sensitivity to market downturns

- Liquidity: Quantified based on token turnover

Factor Model Results

The authors then progressed to construction of a factor model based on the above set of factors, and discussion of the model’s significance and efficacy for the explanation of return variations within the digital asset class.

Given the authors’ substantial integration of the two major approaches for factor model construction within this research, the Fama-French approach, and the Fama-MacBeth approach, a summary of each one is provided, together with important outcomes from their utilisation:

Time-Series Regression

All the aforementioned factors demonstrate significance in a Fama-French setting by effectively capturing the diverse dynamics of cryptocurrency behaviour. Different assets exhibit varying levels of exposure to these factors, underscoring the distinct return drivers unique to each asset.

Cross-Sectional Regression

From the Fama-MacBeth perspective, results align with the preceding observations. All seven risk premia display strong statistical significance, highlighting their importance in explaining cross-sectional asset returns. Moreover, the authors observe significant time variability in these premia, emphasising the dynamic nature of risk pricing throughout the observed period.

Conclusion

The study confirms that Market, Size, Value, Momentum, Growth, Downside Beta and Liquidity factors are relevant for cryptocurrency valuation methodologies. However, the authors also acknowledge that while these factors demonstrate significant capability in capturing risk premia and explaining digital asset returns, a portion of return variance remains unexplained, much like in traditional finance. As such, they further note this underscores the need for additional investigation into factors that could enhance understanding of the unexplained variance.

The authors spotlight traditional finance and crypto-native regime models as areas likely to yield further insights and better understanding of cryptocurrency return variation. The study rounds off the conclusion by noting the research provides a robust foundation for continued exploration of digital asset pricing and risk management.

Click below to download a PDF of the report.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Value and Momentum Outperform in Q2 Rally

The CF Benchmarks' Factor Report applies a robust multi-factor model to digital assets, enabling investors to track key drivers of crypto returns (Market, Size, Value, Momentum, Growth, Downside Beta, and Liquidity) and understand how these factors evolve across different market regimes.

Gabriel Selby

Weekly Index Highlights, July 14, 2025

Crypto's winning streak has extended, with diversified-weight Broad Cap and Large Cap benchmarks up nearly 15%; outpacing ~12% gains by free-float counterparts. ADA and XRP both rose over 20%. Staking yields ticked up, led by SOL's +1%. BTC's realized volatility spiked despite muted implied vol.

CF Benchmarks

Weekly Index Highlights, July 07, 2025

Digital assets gained for a second week, led by Broad and Large-Cap indices up ~2.5%. They outperformed free-float peers, signaling risk-on appetite. Majors rose up to 4%, ETH and NEAR staking yields increased, while BTC volatility stayed near cycle lows.

CF Benchmarks