Apr 04, 2025

Market Outlook: Q2 2025

The New Equilibrium: Unraveling Economic Tension & Thematic Tailwinds

Digital assets are caught in a tug-of-war between promising regulatory developments and challenging economic headwinds. The growth outlook has weakened, with tariff concerns potentially causing a significant drag on GDP. Meanwhile, disinflation appears to be stalling, as inflation expectations diverge sharply. Monetary policy remains constrained, with the Federal Reserve balancing cost-push inflation against labor market softness. Against this backdrop, upcoming stablecoin legislation may offer a regulatory edge for U.S. issuers, while Ethereum’s Pectra upgrade targets improved transaction efficiency and user experience. Bitcoin’s correlation with global M2 highlights its sensitivity to monetary conditions, especially as sovereign debt concerns escalate. Investor appetite continues to favor growth over size, with capital rotating toward established projects as global risk appetite recedes.

Market Summary

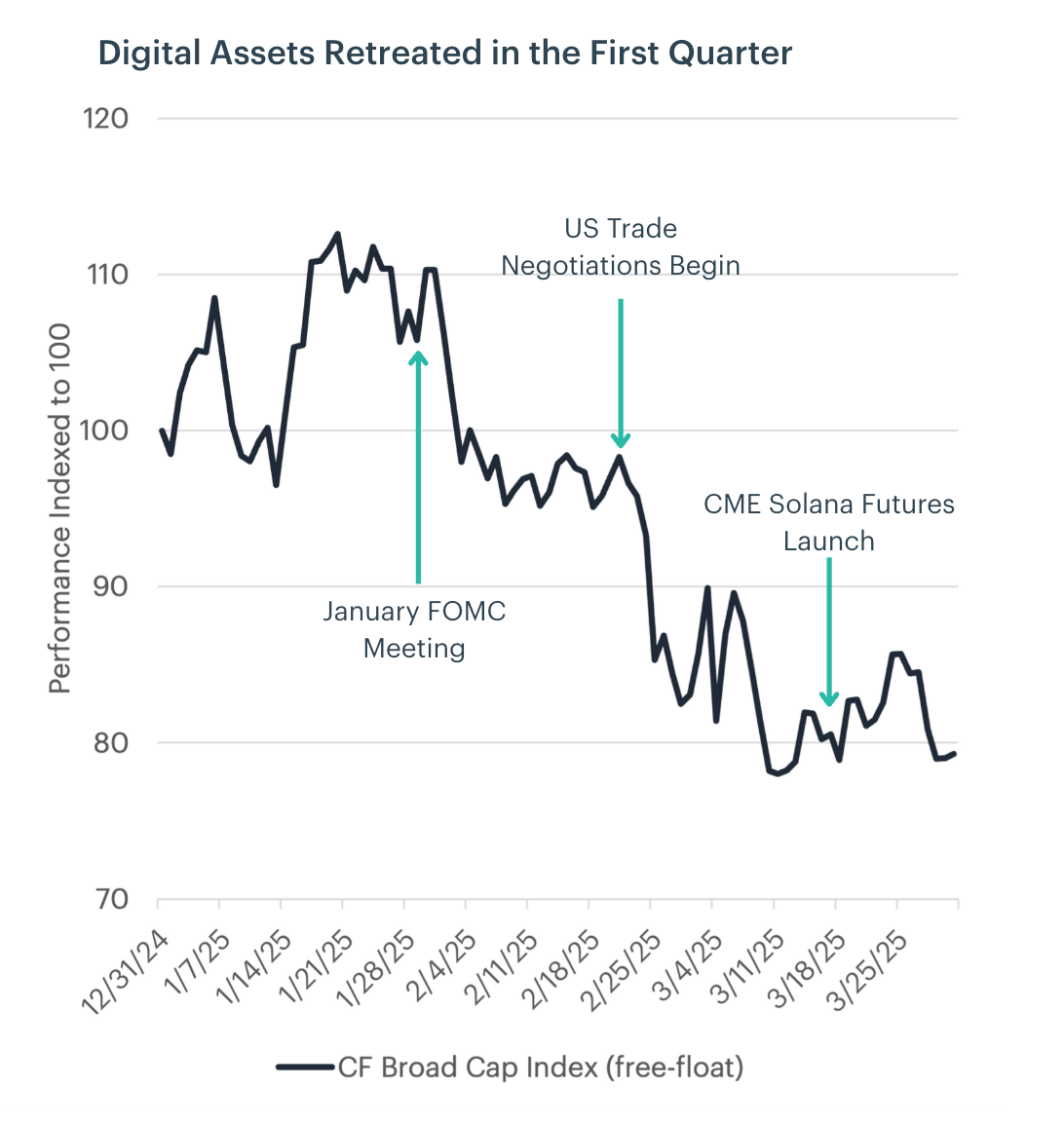

Digital assets began 2025 strongly following positive regulatory developments. In January, President Trump established a Presidential Working Group for digital assets, while the SEC shifted toward crypto-friendly policies by repealing SAB 121 and forming a Crypto Task Force under Commissioner Peirce. These developments propelled Bitcoin above $109,000, setting a new all-time high.

However, mid-quarter market sentiment deteriorated amid macroeconomic uncertainty. Diminished expectations for rate cuts weakened investor confidence, causing Bitcoin to fall below $80,000. A $1.5 billion ByBit security breach and ETF outflows compounded market pressure.

Despite the sell-off, regulatory progress continued as the SEC dropped several high-profile lawsuits against industry participants. CME Group's launch of Solana futures on March 17 expanded regulated crypto derivatives beyond Bitcoin and Ether, benefiting institutional investors. By March, market conditions worsened due to U.S. tariff tensions and disappointing economic data. The Federal Reserve maintained rates while revising growth forecasts downward and raising inflation projections. Stagflation concerns and persistent capital outflows from digital asset ETFs fueled continued volatility across crypto markets.

Macro Backdrop:

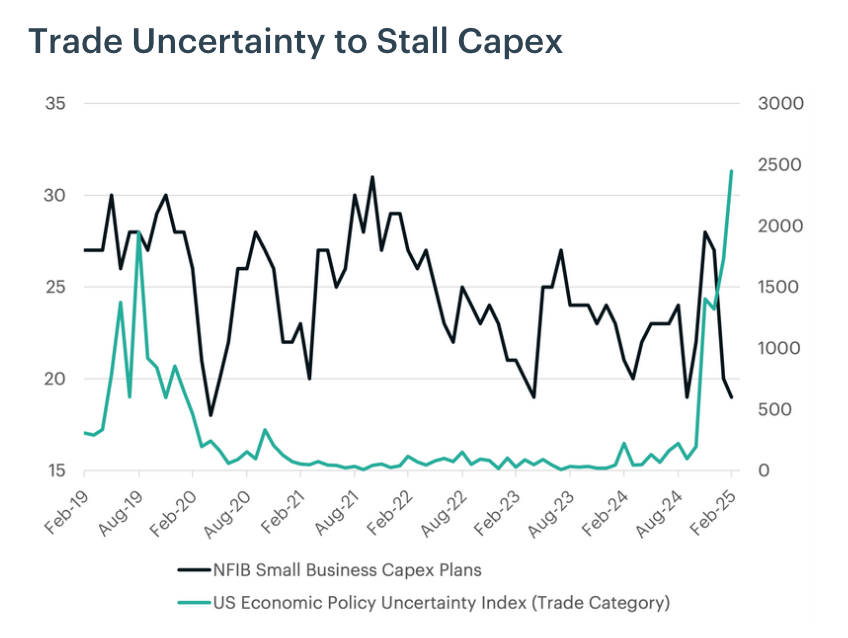

Growth: The U.S. economy faces mounting pressure in Q2 2025 as early post-election optimism fades. Universal 10% tariffs plus reciprocal levies from 60 nations have pushed effective import rates above 20%, creating broad economic drag. External risks from China's property slowdown and emerging market inflation volatility compound concerns. Despite 1.9% GDP growth expectations, high-frequency data shows weakening trends. With tariffs fully implemented, Fed modeling suggests a potential 2.3% GDP drag from the 16-percentage-point tariff increase.

While retail pass-through remains limited, input costs are rising in tariff-exposed sectors. The labor market is softening, with unemployment projections revised upward. Fiscal austerity under DOGE may reinforce demand shock through public sector layoffs, while tax relief and deregulation offer insufficient offset. The outlook remains cautious for 2025's first half, with stagflationary risks rising. Bitcoin appears structurally appealing amid policy ambiguity and dollar debasement concerns.

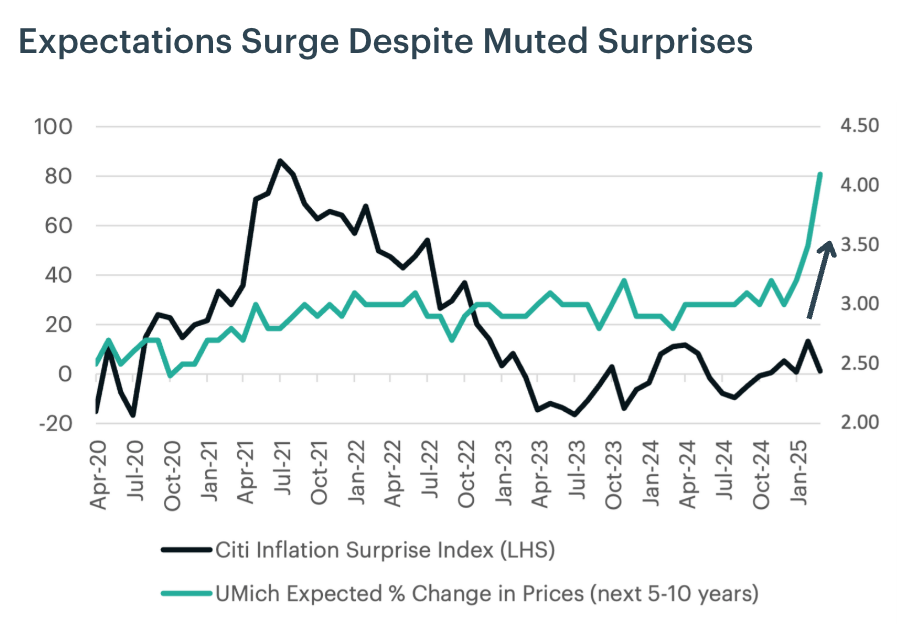

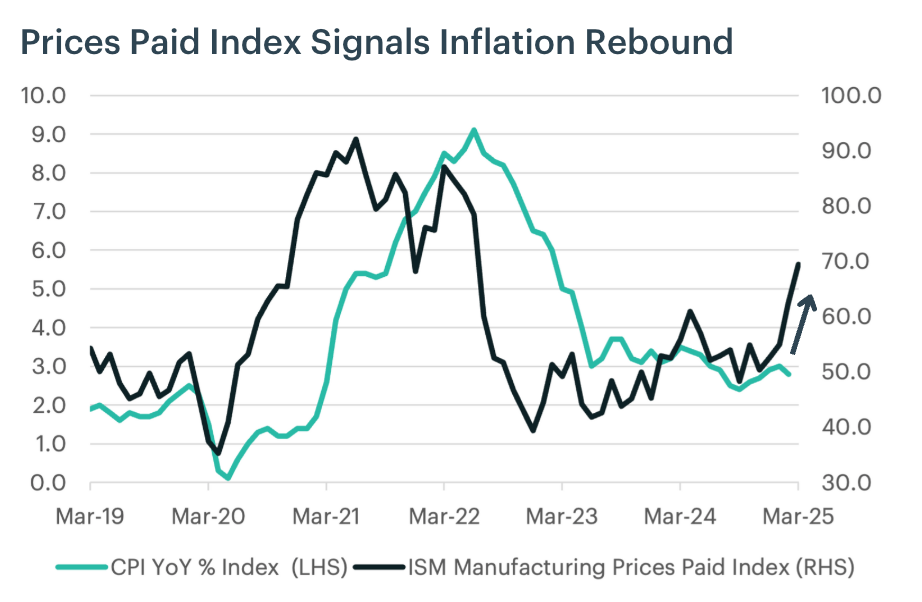

Inflation: The U.S. disinflation narrative faces increasing pressure despite cooler headline readings. The Federal Reserve projects progress, but persistent core inflation, rising commodity costs, and tariff distortions suggest a longer path to the 2% target. Core inflation remains stubborn across services, shelter, and wage-driven components. New tariffs are raising input costs in sectors like autos and electronics, with models suggesting tariffs could boost core PCE inflation by up to 1.5 percentage points in the first year.

Inflation expectations are diverging significantly, with University of Michigan's one-year gauge reaching a 32-year high while the New York Fed's remained anchored. Meanwhile, food and commodity prices are surging due to weather disruptions, fragile supply chains, and trade distortions. Core alternative measures remain elevated above 3.5%. For investors, tactical inflation hedging through sound-money assets is warranted, with Bitcoin potentially benefiting from monetary credibility concerns.

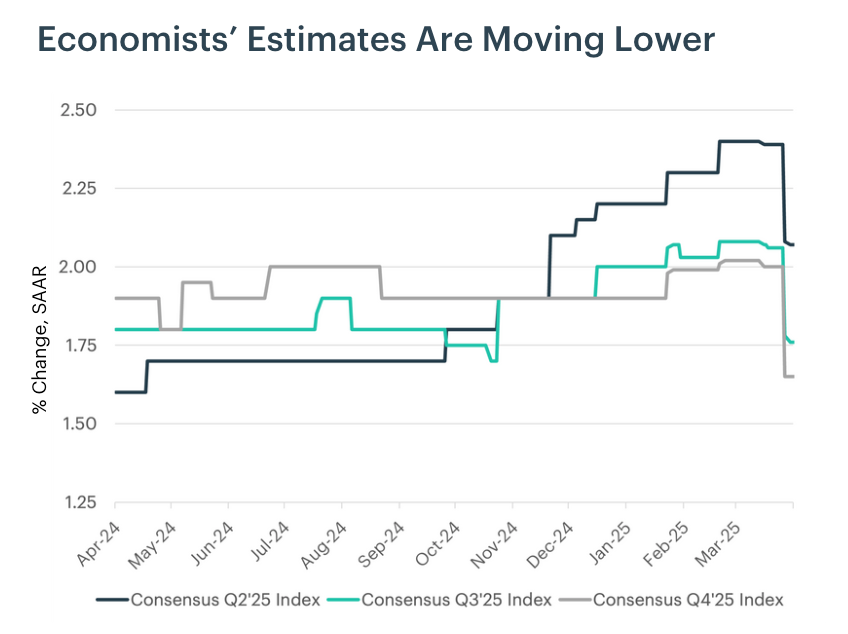

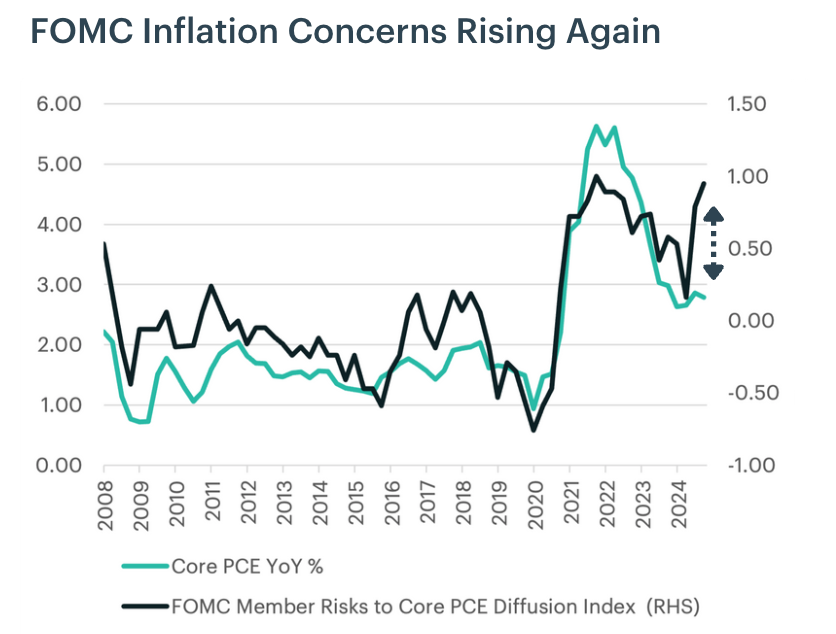

Monetary Policy: Aggressive U.S. trade tariffs have complicated the Federal Reserve's balancing act, introducing cost-push inflation alongside labor market fragility. While the case for easing remains, conviction is wavering amid inflation asymmetry and macro strain. At its March meeting, the FOMC held rates steady and slowed balance sheet runoff. The dot plot still projects two 25-basis-point cuts in 2025, but committee members are split between one and two cuts. Notably, 18 of 19 participants view core PCE risks as tilted upward, pushing the diffusion index to 0.95.

Markets now price 75 basis points of easing this year, up from 50 bps previously. Despite data-dependency, tariff-driven price increases and softening employment leave little policy margin. We now expect a "Fed Put" of 100bps in rate cuts in the latter half of 2025. The monetary backdrop has grown more asymmetric, with weakening growth but intense focus on inflation risks limiting preemptive easing. Yield spikes may force consideration of unconventional stabilization tools.

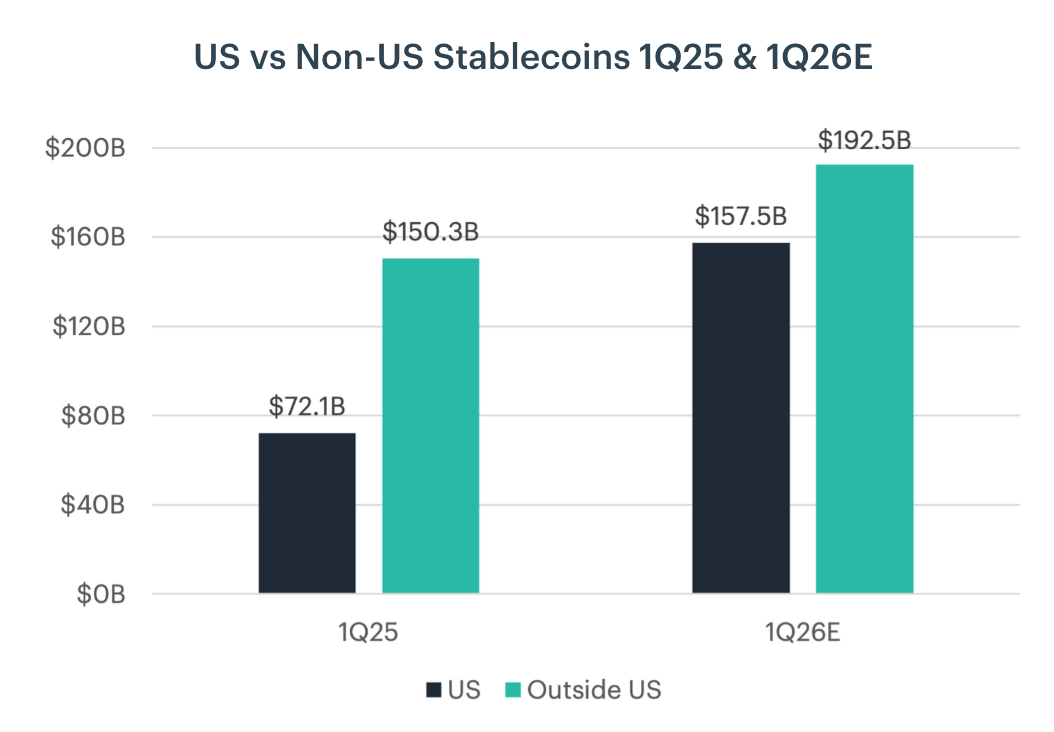

Regulatory Outlook: Two bipartisan bills—the GENIUS Act (Senate) and STABLE Act (House)—are advancing to strengthen the dollar's reserve status. The GENIUS Act, passed by the Senate Banking Committee in March 2025, defines payment stablecoins, mandates 1:1 reserve backing, audits, and federal licensing for large issuers. The STABLE Act, cleared by the House Financial Services Committee in April 2025, requires similar provisions. Both aim to give US issuers competitive advantage.

Stablecoin legislation is expected to pass before August recess, potentially increasing US issuers' global market share from 30% to 45% within a year, while consolidating the market around larger players. A market structure bill following August recess will establish clear regulatory oversight between the CFTC and SEC for digital assets. This regulatory clarity should attract capital and new participants, positioning the US as the leader in the crypto landscape. Meanwhile, Ethereum currently hosts most stablecoin activity, though other smart contract platforms also stand to benefit.

Secular Themes

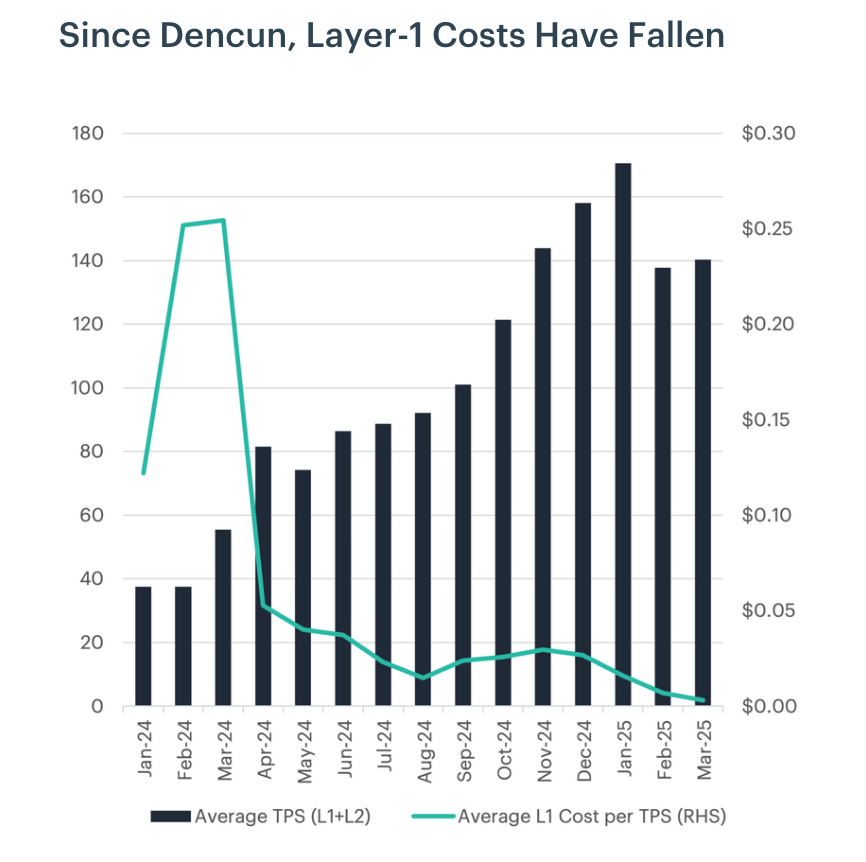

Network Upgrades: The upcoming Ethereum upgrade, Pectra, aims to address user complaints by enhancing UX and enabling cost reductions for Layer 2 solutions. By increasing blob transaction limits, Pectra will solidify Ethereum's Layer 1 leadership. Account abstraction (EIP-7702) simplifies user experience by allowing wallets to pay transaction fees using stablecoins, removing the need to hold ETH for fees. Smart contract optimizations (EIP-7692) enhance EVM efficiency and reduce gas costs, while increased blob capacity drives further cost reductions.

Changes to staking in Pectra will encourage greater participation by raising the validator cap from 32 ETH to 2048 ETH, decreasing validators while improving consensus. EIP-6110 introduces faster validator activation, addressing liquidity concerns. Following the Dencun upgrade in April, Ethereum's combined L1+L2 throughput has climbed while average L1 transaction costs have dropped, suggesting additional network capacity is available ahead of Pectra's UX enhancements. Pectra's improvements are expected to attract new users, complementing proposed stablecoin and market structure bills.

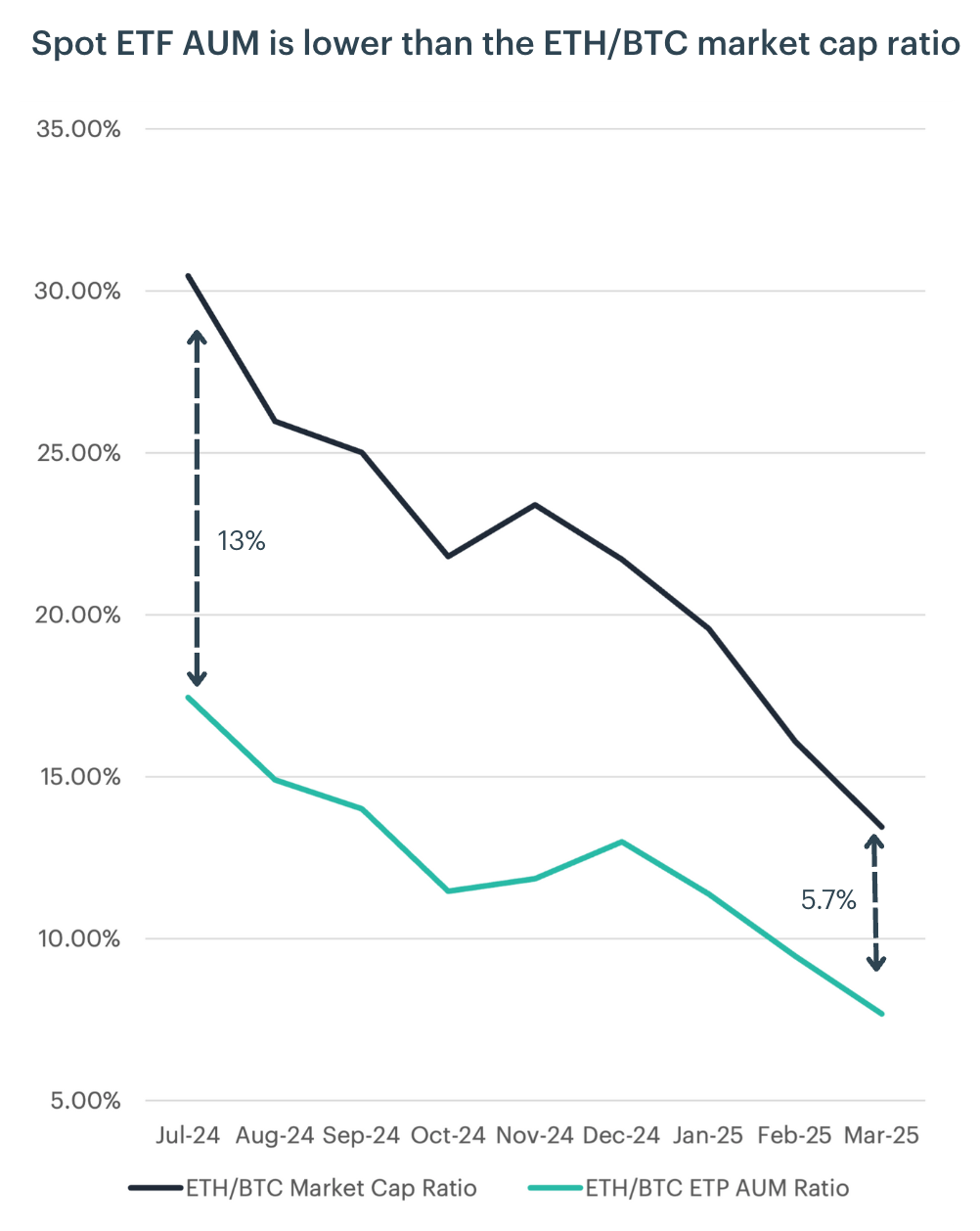

Institutional Adoption: While Bitcoin ETFs prompted significant inflows, Ethereum ETFs haven't seen similar adoption largely because current spot Ether ETFs lack staking functionality. Staking is crucial to Ethereum's total return, allowing holders to earn newly minted ETH and network fees.

In early 2025, both NYSE and CBOE submitted filings to incorporate staking into spot Ether ETFs. This addition could catalyze significant inflows, similar to Bitcoin's post-ETF financialization trend.

Currently, Ethereum's market capitalization is approximately 13.5% of Bitcoin's, yet Ether ETPs hold only 7.7% of assets under management compared to Bitcoin-based ETPs. Enabling staking could close this gap, potentially shrinking the difference between Ether's share of ETP AUM and market capitalization from 5.7% to less than 3% within twelve months of approval. Looking ahead, staking in ETFs could push Ethereum's staked supply above 30% from the current 28%, potentially lowering staking yields while improving overall liquidity and institutional appeal.

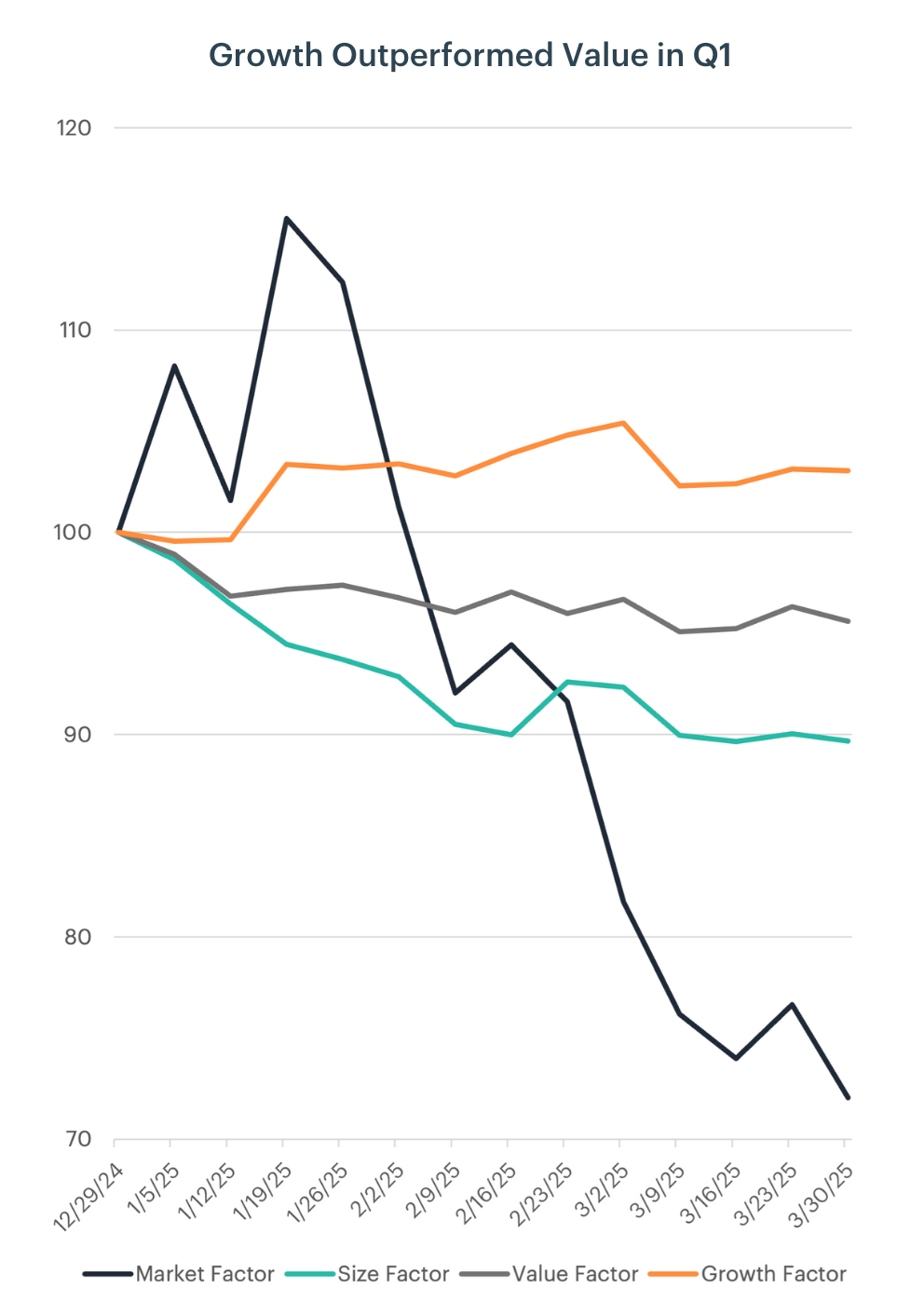

Factor Performance: In Q1, the growth factor outperformed while value lagged. The size factor underperformed as the structure of holding long small-cap positions while shorting larger-cap assets exposed it to recent small-cap underperformance. Within the growth factor, performance was driven by holding high-growth tokens with robust fee growth and strong daily active user metrics, while shorting assets with slow or negative growth trajectories. This approach proved effective during recent market volatility.

Looking ahead, the size factor will likely continue underperforming in 2025 as macroeconomic conditions shift. Capital has rotated away from newer projects, typically more prevalent among small-caps, as investors seek safety. A resurgence of the value factor is anticipated as market participants become more selective, with demand rising for tokens with larger user bases and higher total value locked on-chain. In the current risk-off regime, market cap or free-float weighted indices favoring large-cap tokens should outperform more diversified indices with small-cap tilt.

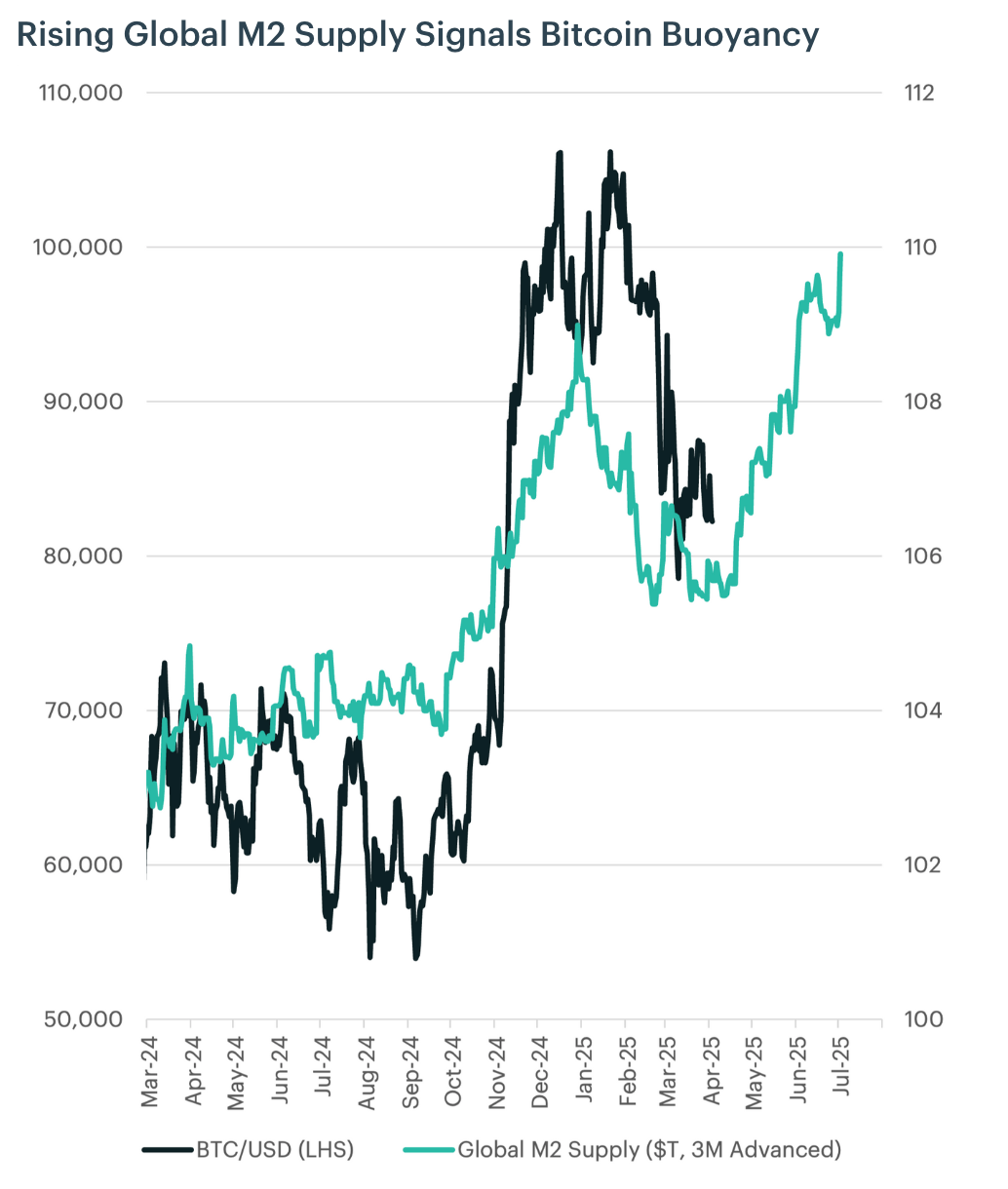

Global Liquidity: Global liquidity trends may play a defining role in shaping digital asset performance in 2025. Bitcoin has historically shown strong sensitivity to changes in global M2 money supply, with expansions often preceding rallies and contractions correlating with drawdowns. Bitcoin's decline from its $109K January peak to $78K by early March coincided with global M2 contraction from $107.2T to $106.5T, reinforcing its role as a high-beta macro asset. With M2 supply now stabilizing, a potential inflection point may be forming.

While Bitcoin's structural case remains intact, near-term performance will continue to be influenced by global liquidity trajectories. If major central banks pivot toward easing in response to slowing growth or disinflation, renewed M2 expansion could provide tailwinds. Bitcoin's role as a hedge against monetary debasement may gain renewed attention as sovereign debt burdens rise, making it increasingly attractive as traditional currencies face purchasing power erosion.

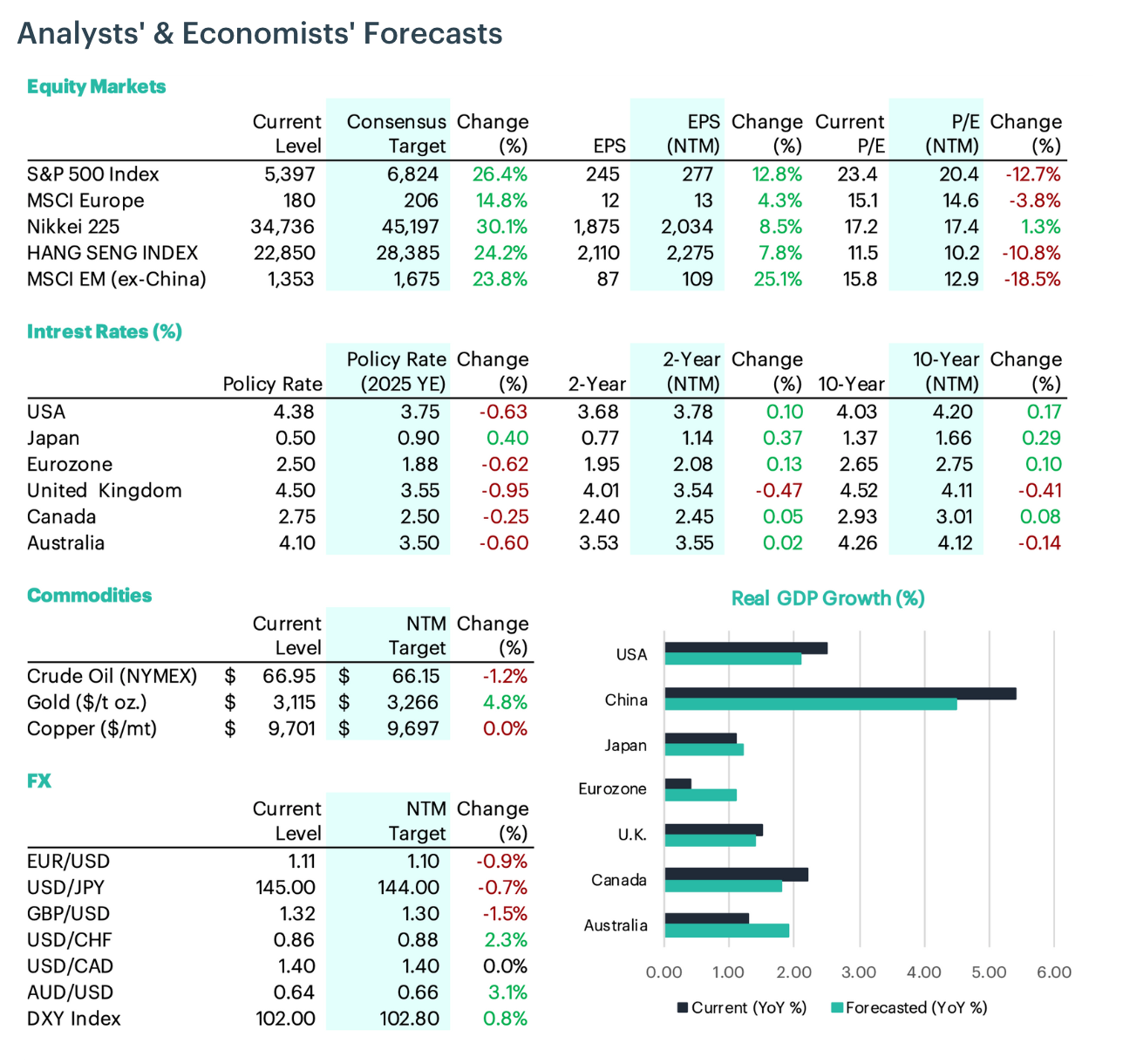

Asset Class Overview & Forecasts:

Equities: Analysts project positive returns across regions, with Japanese stocks leading (30.1%), followed by Chinese (26.4%) and Hong Kong (24.2%). Emerging markets ex-China and U.S. equities are forecast at 23.8% and 26.4% respectively, while European equities lag at 14.8%.

Interest Rates: Markets anticipate meaningful cuts across developed economies, with the UK and Eurozone leading. The U.S., Australia, and Canada expected to cut by 0.63%, 0.60%, and 0.25%, while Japan may increase by 0.40%.

Commodities: Gold is expected to rise 4.8% to $3,266/oz, crude oil to decline 1.2% to $66.15/barrel, with copper prices remaining flat.

FX: USD expected to remain stable with DXY rising 0.8%. Modest currency moves projected across major pairs.

GDP Growth: Regional divergence continues with China leading at 4.5%, followed by U.S. and Australia, while Japan, Canada, Eurozone and U.K. show lower growth.

To read the our full market outlook report, please click here.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Value and Momentum Outperform in Q2 Rally

The CF Benchmarks' Factor Report applies a robust multi-factor model to digital assets, enabling investors to track key drivers of crypto returns (Market, Size, Value, Momentum, Growth, Downside Beta, and Liquidity) and understand how these factors evolve across different market regimes.

Gabriel Selby

Weekly Index Highlights, July 14, 2025

Crypto's winning streak has extended, with diversified-weight Broad Cap and Large Cap benchmarks up nearly 15%; outpacing ~12% gains by free-float counterparts. ADA and XRP both rose over 20%. Staking yields ticked up, led by SOL's +1%. BTC's realized volatility spiked despite muted implied vol.

CF Benchmarks

Weekly Index Highlights, July 07, 2025

Digital assets gained for a second week, led by Broad and Large-Cap indices up ~2.5%. They outperformed free-float peers, signaling risk-on appetite. Majors rose up to 4%, ETH and NEAR staking yields increased, while BTC volatility stayed near cycle lows.

CF Benchmarks